One of the biggest myths in home buying is that there’s only one way to get a mortgage. In reality, there are several loan options — and the best option for you depends on your credit, savings, location, and life situation.

In today’s rate environment, structure matters more than ever. The right loan can save (or cost) you tens of thousands over time.

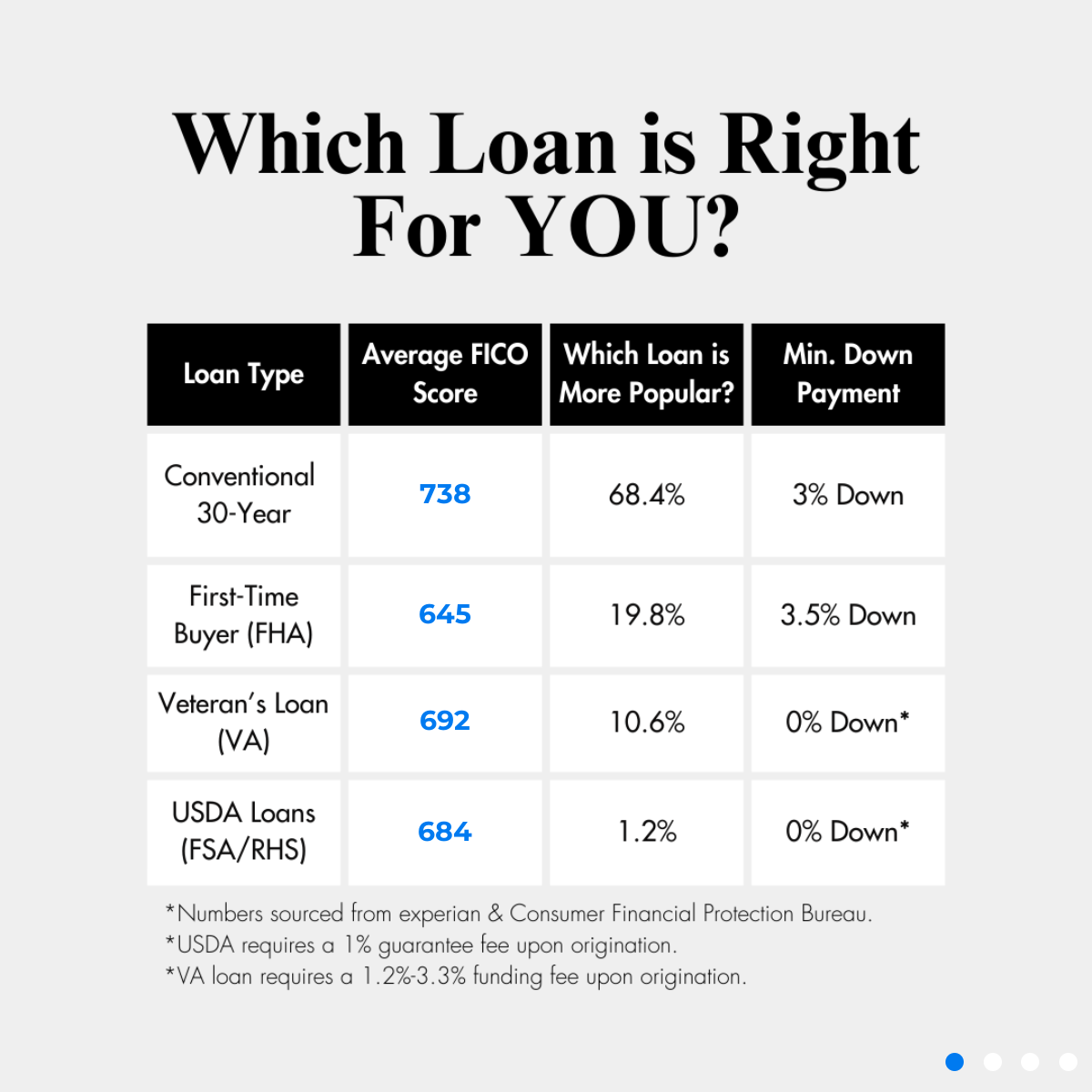

Let’s break down the four most common home loans in plain English and talk about which one serves you best!

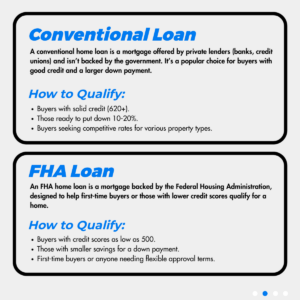

1. Conventional Loan (30-Year)

Best for: Buyers with strong credit and some savings

A conventional loan is offered by private lenders (not backed by the government).

Typical Snapshot:

- Minimum down payment: 3% (but many put down more)

- Most widely used loan type

Great fit for:

✔ Buyers with good-to-excellent credit (usually 620+)

✔ Those who can put down 5–20%

✔ Buyers who want competitive interest rates

✔ People purchasing a variety of property types (primary homes, second homes, etc.)

Things to know:

- If you put down less than 20%, you’ll pay Private Mortgage Insurance (PMI) — but it can be removed later once you build equity.

- Strong financial profiles usually get the best terms.

👉 Bottom line: If you qualify comfortably, this is often the strongest long-term wealth-building option.

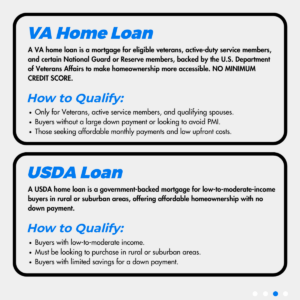

2. VA Loan (For Veterans & Service Members)

Best for: Eligible veterans, active-duty military, and qualifying spouses

VA loans are backed by the U.S. Department of Veterans Affairs and are one of the most powerful benefits available to those who’ve served.

Typical Snapshot:

- Average credit score: No official minimum set by the VA; however lenders prefer 580 – 620+

- Down payment: 0% required

- No monthly mortgage insurance

Great fit for:

✔ Veterans and active service members

✔ Buyers who want to avoid a large down payment

✔ Those looking for lower upfront costs

✔ Buyers wanting to avoid PMI

Things to know:

- There is a VA funding fee (typically 1.2%–3.3%), but it can often be rolled into the loan.

- More flexible credit guidelines than conventional loans.

- Property condition standards can be stricter.

👉 Bottom line: If you qualify, VA is often the most powerful loan structure available — especially if saving for a down payment has been a challenge.

3. USDA Loan (Rural & Suburban Buyers)

Best for: Moderate income buyers in eligible rural or suburban areas.

USDA loans are government-backed and designed to make homeownership more accessible outside major metro centers.

Typical Snapshot:

- Down payment: 0% required

- Location must qualify

Great fit for:

✔ Buyers with limited savings

✔ Households with low-to-moderate income

✔ Homes located in eligible rural or suburban areas

Things to know:

- There are income limits based on area and household size.

- A USDA guarantee fee applies (about 1% upfront).

- Not every property qualifies — location matters.

👉 Bottom line: If you’re open to living outside city centers and don’t make more than the published maximum in income, this can dramatically reduce upfront cash needed.

4. FHA Loan (First-Time & Credit-Challenged Buyers)

Best for: First-time buyers or those with lower credit scores

FHA loans are backed by the Federal Housing Administration and are designed to help more people qualify.

Typical Snapshot:

- Down payment: As low as 3.5%

- Credit scores can qualify as low as 500 (with higher down payment).

Great fit for:

✔ Buyers with lower credit scores

✔ Those with smaller savings

✔ First-time buyers

✔ People needing more flexible approval guidelines

Things to know:

- FHA loans require Mortgage Insurance Premium (MIP), which often lasts for the life of the loan unless refinanced.

- Easier to qualify for, but long-term costs can be higher than conventional.

👉 Bottom line: FHA can be a great stepping stone into homeownership when credit or savings aren’t quite where you want them yet.

So… How do you choose?

Start with a Pre-Approval. A real pre-approval doesn’t just tell you what you qualify for, it shows:

- Monthly payment differences

- Upfront cash required

- Long-term cost comparison

- Exit strategy (refinance or removal of mortgage insurance)

Final Thought

The “best” loan isn’t the one with the flashiest feature — it’s the one that fits your financial picture, goals, and timeline.

The “best” loan isn’t the one with the flashiest feature — it’s the one that fits your financial picture, goals, and timeline.

Before you write an offer, let me refer you to a lender that can compare your options side-by-side. A good lender (and a knowledgeable real estate professional) show you the following:

- Your monthly payment

- Your upfront costs

- Your long-term savings.

That’s how you protect your money.

If you’d ever like help understanding how these options apply to your situation, I’m always happy to connect you with trusted lending professionals and help you map out the smartest path to homeownership.

Give GranburyOne Realty Team a call today!

Information acquired with assistance from McDaniel Mortgage.

Graphics by: Palm Agent